How I Smartly Planned for Cosmetic Surgery — And Kept My Finances Intact

So you’re thinking about cosmetic surgery? Yeah, me too — and I quickly realized it’s not just about picking a surgeon. The real challenge? Paying for it without wrecking your financial life. I went through the stress of hidden fees, surprise costs, and payment panic. But I found a smarter way. This is how I planned ahead, protected my budget, and still got the results I wanted — without financial regrets. It wasn’t about cutting corners or taking risks with my money. It was about treating the decision with the seriousness it deserved — as both a personal and financial milestone. Like buying a home or saving for a child’s education, cosmetic surgery requires preparation, discipline, and long-term thinking. And just like any major life expense, the key to success lies not in the procedure itself, but in how well you prepare for it.

The Real Cost of Looking "Perfect"

Cosmetic surgery is often marketed as a straightforward path to confidence, but behind the glossy brochures and before-and-after photos lies a complex financial reality. The upfront price quoted during an initial consultation is rarely the full story. While some clinics advertise rhinoplasty starting at $3,000 or liposuction from $2,500, these figures typically cover only the surgeon’s fee. Additional costs — many of which are essential — include anesthesia, facility fees, pre-operative lab work, post-surgical garments, prescription medications, and follow-up visits. In some cases, patients may require revision procedures or extended recovery support, further increasing the total expense. For example, a seemingly simple eyelid lift can quickly escalate from $3,000 to over $5,000 once all associated services are factored in.

What makes this financial landscape especially challenging is the lack of standardization across providers. One clinic might bundle anesthesia and facility charges into a single quote, while another lists them separately, creating confusion and making accurate comparisons difficult. I learned this firsthand when I received three different quotes for the same procedure — each with a different breakdown of costs. The lowest initial price turned out to be the most expensive in the end due to unlisted fees. This experience taught me that transparency matters. A responsible provider should be willing to give a detailed, itemized estimate that includes every anticipated charge. If they hesitate or offer vague answers, that’s a red flag.

Understanding the full scope of expenses isn’t just about budgeting — it’s about protecting your financial stability. Taking on unexpected costs after surgery can strain household finances, delay other important goals like saving for retirement or paying off debt, or even lead to reliance on high-interest credit. That’s why it’s crucial to treat cosmetic surgery not as a spontaneous purchase but as a planned financial commitment. By mapping out every potential cost in advance, you gain control over the process and reduce the risk of unpleasant surprises. This level of preparation transforms what could be a source of stress into a manageable, well-structured goal.

Why Emotional Spending Leads to Financial Regret

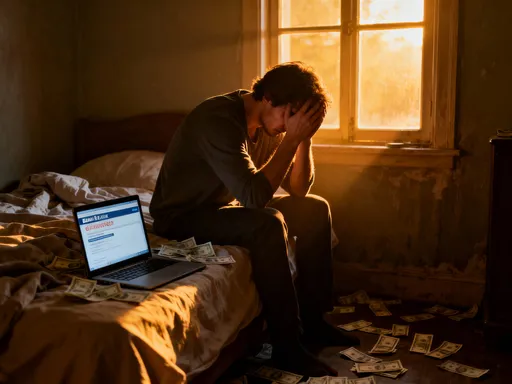

It’s no secret that cosmetic surgery is often rooted in emotional motivation. Whether it’s a desire to feel more confident, recover a sense of self after weight loss, or address a feature that’s bothered you for years, the decision frequently stems from personal feelings rather than practical necessity. While these motivations are valid, they can also cloud financial judgment. When emotions drive spending, we tend to focus on immediate desires rather than long-term consequences. I made this mistake when I scheduled a minor facial procedure shortly after going through a difficult family situation. At the time, it felt like a way to reclaim control and feel better about myself. But within weeks, I began questioning whether the surgery was truly necessary or simply a reaction to temporary stress.

This emotional spending pattern is common and can lead to lasting financial regret. Studies in behavioral finance show that people are more likely to make impulsive financial decisions during periods of emotional upheaval. The brain’s reward system becomes activated by the promise of quick improvement, overshadowing rational evaluation of cost, risk, and necessity. In the context of cosmetic surgery, this can mean agreeing to a procedure without fully researching alternatives, comparing prices, or considering whether the timing aligns with one’s financial readiness. The result? A physical change that may bring short-term satisfaction but leaves behind lingering anxiety about the financial burden.

To avoid this trap, I adopted a cooling-off period before making any final decisions. I set a rule: no appointments or deposits until at least three months after my initial consultation. During that time, I revisited my reasons for wanting the procedure, discussed it with a trusted friend, and reviewed my financial plan. I also consulted a financial advisor, not for investment advice, but to assess how the expense would impact my overall budget and long-term goals. This pause allowed me to separate emotional desire from practical necessity. By the time I moved forward, I was confident that the decision was thoughtful, not reactive. Emotional well-being matters — but so does financial peace of mind.

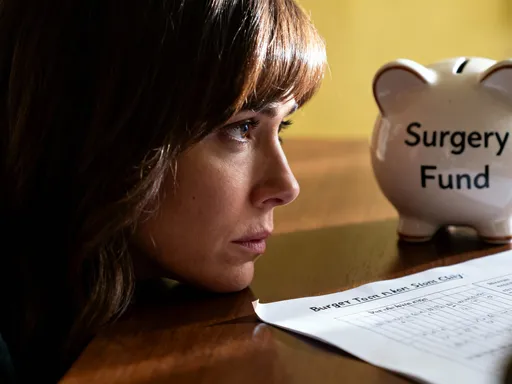

Building a Dedicated Surgery Fund: Pay Yourself First

Once I committed to moving forward — and only after I was emotionally and financially ready — I began building a dedicated fund for the surgery. Instead of relying on credit cards or loans, I treated the expense like any other major life goal: systematically and with discipline. I opened a high-yield savings account specifically labeled “Surgery Fund” and set up automatic monthly transfers from my checking account. This “pay yourself first” approach ensured that saving for the procedure became a priority, not an afterthought. Every paycheck, a fixed amount went directly into the fund, just like retirement contributions or a mortgage payment.

The psychological benefit of this strategy was just as important as the financial one. Watching the balance grow over time gave me a sense of progress and control. It transformed an abstract goal into a tangible reality. There were months when I had to tighten my budget — skipping a weekend trip or delaying a home upgrade — but knowing that every sacrifice brought me closer to my objective made it worthwhile. More importantly, by saving in advance, I eliminated the need for debt. Paying in cash meant no interest charges, no monthly payments, and no risk of falling behind if unexpected expenses arose elsewhere.

This method also reinforced healthy financial habits. Because I was already accustomed to setting aside money each month, transitioning the fund to another goal after the surgery felt natural. Once the procedure was complete, I redirected the same monthly amount toward retirement savings and emergency fund contributions. The discipline I developed during the saving phase didn’t end with the surgery — it became a permanent part of my financial routine. Treating cosmetic surgery as a planned expenditure, rather than an impulsive purchase, not only protected my budget but strengthened my overall financial resilience.

Comparing Payment Options: Cash, Financing, and Medical Loans

While paying in full with cash is ideal, it’s not always feasible for everyone. For those who need financing, the options can be overwhelming — and potentially risky if not carefully evaluated. I spent weeks researching medical credit cards, personal loans, and clinic-specific payment plans to understand the trade-offs. Each option has its advantages, but also significant drawbacks that must be weighed against your financial situation.

Medical credit cards, such as CareCredit, are widely advertised and often promoted by clinics. They typically offer deferred interest plans — meaning no interest is charged if the balance is paid in full within a set period, usually 12 to 24 months. While this sounds appealing, the risk is substantial: if even one payment is missed or the balance isn’t fully repaid by the deadline, interest is applied retroactively to the original purchase amount. This can result in hundreds or even thousands of dollars in unexpected charges. I knew someone who fell into this trap and ended up paying nearly double the procedure cost due to a single late payment.

Personal loans from banks or credit unions offer a more predictable alternative. These typically come with fixed interest rates and set repayment terms, making it easier to budget monthly payments. Unlike medical credit cards, there’s no deferred interest — you know exactly how much you’ll pay over time. I compared several lenders and chose a five-year fixed-rate loan with a moderate APR. The monthly payments were manageable, and the total repayment cost was transparent from the start. Clinic financing plans, while convenient, often come with higher interest rates or less favorable terms, so I approached them with caution.

The key to making a smart financing decision is reading the fine print and calculating the total cost of repayment, not just the monthly payment. It’s easy to be drawn in by low monthly figures, but those can be misleading if the loan term is long or the interest rate is high. I used online loan calculators to compare scenarios and ensure I wasn’t underestimating the long-term impact. Ultimately, financing should never stretch your budget to the breaking point. If the numbers don’t work without compromising essential expenses or emergency savings, it’s a sign to wait and save longer.

Timing the Procedure for Maximum Financial Advantage

One of the most overlooked aspects of financial planning for cosmetic surgery is timing. When you schedule the procedure can have a meaningful impact on cost, cash flow, and overall stress. I discovered that many clinics offer promotional pricing during slower seasons — typically late winter or early fall — when demand is lower. By scheduling my surgery in February, I qualified for a 10% discount that wasn’t available during peak months like May or September. Some providers also run year-end specials to meet revenue targets, creating opportunities for savings if you’re flexible with your timeline.

Aligning the surgery with my income cycle was another strategic move. I planned the procedure to coincide with my annual bonus and tax refund, which together covered nearly half the total cost. This approach allowed me to minimize withdrawals from my regular budget and avoid disrupting other financial goals. It also reduced the need for financing, since a large portion of the expense was covered by windfall income rather than ongoing cash flow.

Timing also affects non-financial costs, particularly lost income during recovery. If you’re not on paid medical leave, taking time off work means a temporary drop in household earnings. I scheduled my surgery during a low-stress period at work, when deadlines were light and vacation days were easier to take. This minimized professional disruption and made the recovery process less stressful. For self-employed individuals or those without paid leave, this factor is even more critical. Planning the surgery during a seasonal lull or slow business period can help maintain income stability. Smart timing isn’t about waiting for perfection — it’s about aligning the procedure with your financial and personal rhythms for the best possible outcome.

Protecting Your Budget: Emergency Buffers and Hidden Costs

No matter how carefully you plan, unexpected expenses can arise. One of my closest friends underwent a routine breast augmentation and experienced prolonged swelling that required additional ultrasound therapy — a service not included in her original quote. Because she hadn’t budgeted for contingencies, she had to use her credit card to cover the extra cost, which delayed her ability to pay off the initial surgery balance. Her experience was a wake-up call for me. I realized that every surgery budget should include a buffer for unforeseen circumstances.

I added a 15–20% emergency fund to my total estimated cost to account for potential overages. This covered everything from prescription pain medication and compression garments to unexpected follow-up visits or extended recovery time. Some clinics charge extra for post-op care packages, while others may recommend supplements or specialized skincare products that aren’t part of the standard quote. These costs may seem minor individually, but they can add up quickly.

Treating the surgery budget like a project with built-in contingencies made the entire process more realistic and less stressful. I also researched my surgeon’s policy on revision procedures — some include one follow-up correction at no additional cost, while others charge full price. Knowing this in advance helped me assess not just the initial price, but the long-term value of the service. Just as homeowners set aside money for repairs or car owners budget for maintenance, patients should anticipate that cosmetic surgery may require additional investment. Building a financial cushion isn’t pessimistic — it’s prudent. It ensures that a minor complication doesn’t become a major financial setback.

Long-Term Financial Health: Beyond the Surgery

Completing the surgery wasn’t the end of my financial journey — it was a transition point. Once recovery was underway, I made a deliberate choice not to stop saving. Instead, I re-allocated the monthly amount I had been setting aside for the surgery fund toward long-term goals like retirement and investment accounts. This helped maintain the habit of disciplined saving and prevented lifestyle inflation — the tendency to spend more once a major expense is behind you. The mindset shift was powerful: I wasn’t just funding a one-time procedure, I was building a sustainable financial routine.

I also reviewed my health insurance policy to understand what, if anything, would be covered in the event of complications. While elective cosmetic procedures are typically excluded, some policies may cover medically necessary interventions if issues like infection, scarring, or functional impairment arise. Knowing the limits of my coverage gave me peace of mind and helped me assess risk more realistically. I even considered adding a supplemental health plan for greater protection, though I ultimately decided the added cost wasn’t justified given my overall health and the low risk of complications.

Looking back, the most significant transformation wasn’t just physical — it was financial. I gained confidence not only in my appearance but in my ability to make thoughtful, responsible decisions. True financial health isn’t measured solely by account balances or investment returns. It’s reflected in the choices we make when no one is watching — when we prioritize long-term security over short-term gratification. Cosmetic surgery was a personal goal, but the planning process taught me broader lessons about discipline, patience, and aligning spending with values. The result? A stronger body, a clearer mind, and a healthier bank account.

Planning for cosmetic surgery isn’t just about vanity — it’s about responsibility. By treating it as a serious financial decision, not an impulse buy, I avoided debt, reduced stress, and achieved my goal on my terms. The real transformation wasn’t just physical — it was financial clarity. When you align your spending with your values and plan with purpose, you don’t just look better. You feel better — all the way to your bank account.